This web page was created programmatically, to learn the article in its authentic location you possibly can go to the hyperlink bellow:

https://stockstory.org/us/stocks/nasdaq/swim/news/earnings/latham-nasdaqswim-reports-sales-below-analyst-estimates-in-q1-cy2026-earnings

and if you wish to take away this text from our website please contact us

Residential swimming pool producer Latham (NASDAQ:SWIM) missed Wall Street’s income expectations in Q1 CY2026, however gross sales rose 5.3% 12 months on 12 months to $117.3 million. On the opposite hand, the corporate’s outlook for the complete 12 months was near analysts’ estimates with income guided to $595 million on the midpoint. Its GAAP lack of $0.07 per share was according to analysts’ consensus estimates.

Is now the time to purchase Latham? Find out in our full analysis report.

Latham (SWIM) Q1 CY2026 Highlights:

- Revenue: $117.3 million vs analyst estimates of $119.2 million (5.3% year-on-year progress, 1.6% miss)

- EPS (GAAP): -$0.07 vs analyst estimates of -$0.07 (in line)

- Adjusted EBITDA: $12.16 million vs analyst estimates of $12.88 million (10.4% margin, 5.6% miss)

- The firm reconfirmed its income steering for the complete 12 months of $595 million on the midpoint

- EBITDA steering for the complete 12 months is $112.5 million on the midpoint, above analyst estimates of $110.4 million

- Operating Margin: -5.6%, down from -4.4% in the identical quarter final 12 months

- Free Cash Flow was -$58.22 million in comparison with -$50.33 million in the identical quarter final 12 months

- Market Capitalization: $678.4 million

Commenting on the outcomes, Sean Gadd, President and CEO, mentioned, “We proceed to execute successfully on our strategic priorities and achieved gross sales progress in every of our product strains within the first quarter. Sales progress was led by beneficial properties in autocovers and liners and the advantages of the Freedom Pools acquisition, whereas opposed climate situations in North America saved natural in-ground pool gross sales regular year-over-year. Adjusted EBITDA progress outpaced gross sales progress by a substantial margin, demonstrating Latham’s substantial working leverage and value self-discipline, which greater than offset the impression of upper investments in progress initiatives.

Company Overview

Started as a household enterprise, Latham (NASDAQ:SWIM) is a world designer and producer of in-ground residential swimming swimming pools and associated merchandise.

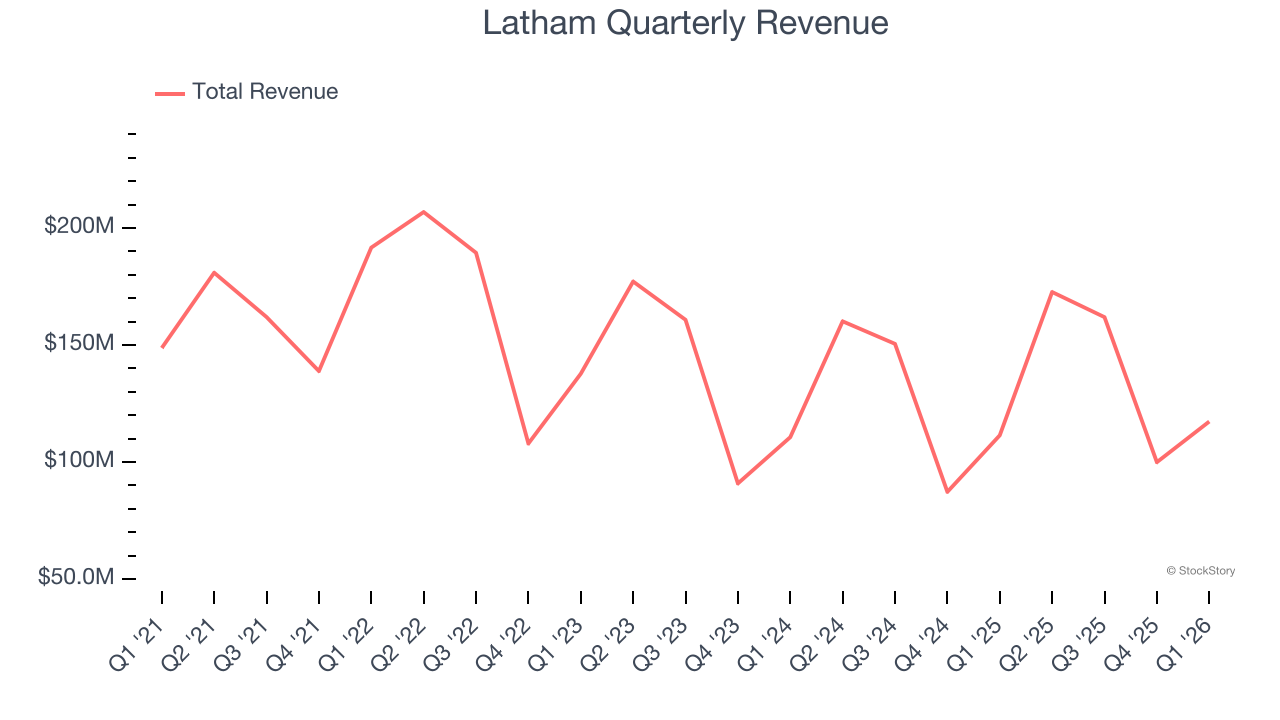

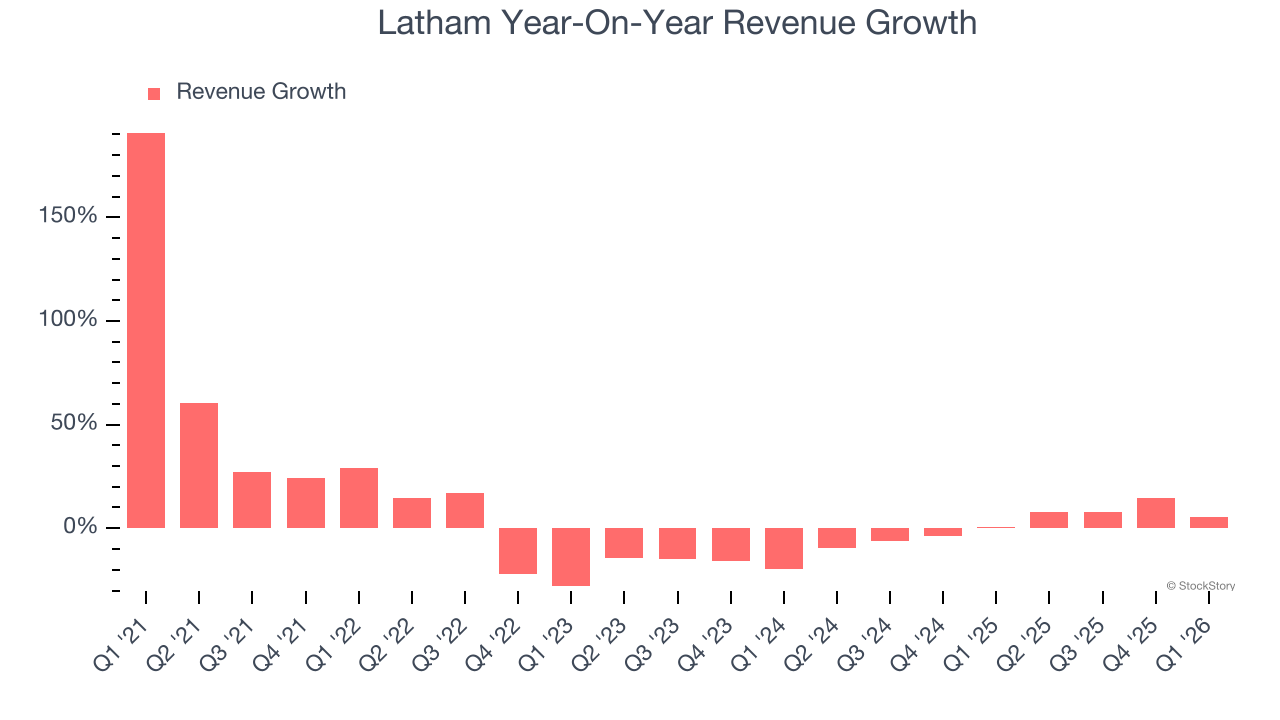

Revenue Growth

Reviewing an organization’s long-term gross sales efficiency reveals insights into its high quality. Any enterprise can have short-term success, however a top-tier one grows for years. Over the final 5 years, Latham grew its gross sales at a weak 2% compounded annual progress charge. This was beneath our requirements and is a tough place to begin for our evaluation.

We at StockStory place probably the most emphasis on long-term progress, however inside client discretionary, a stretched historic view might miss an organization using a profitable new product or development. Latham’s annualized income progress of 1.1% over the past two years aligns with its five-year development, suggesting its demand was constantly weak.

This quarter, Latham’s income grew by 5.3% 12 months on 12 months to $117.3 million, lacking Wall Street’s estimates.

Looking forward, sell-side analysts count on income to develop 9.2% over the subsequent 12 months. Although this projection signifies its newer services will catalyze higher top-line efficiency, it’s nonetheless beneath common for the sector.

WHILE YOU’RE HERE: The Next Palantir? One satellite tv for pc firm captures photos of each level on Earth. Every single day. The Pentagon desires it. Hedge funds are utilizing it to beat earnings. You’ve in all probability by no means heard of it.

This is what the early days of Palantir regarded like earlier than it turned a $437 billion big. Same playbook. Different know-how. If you missed Palantir, you must see this. Claim The Stock Ticker for Free HERE.

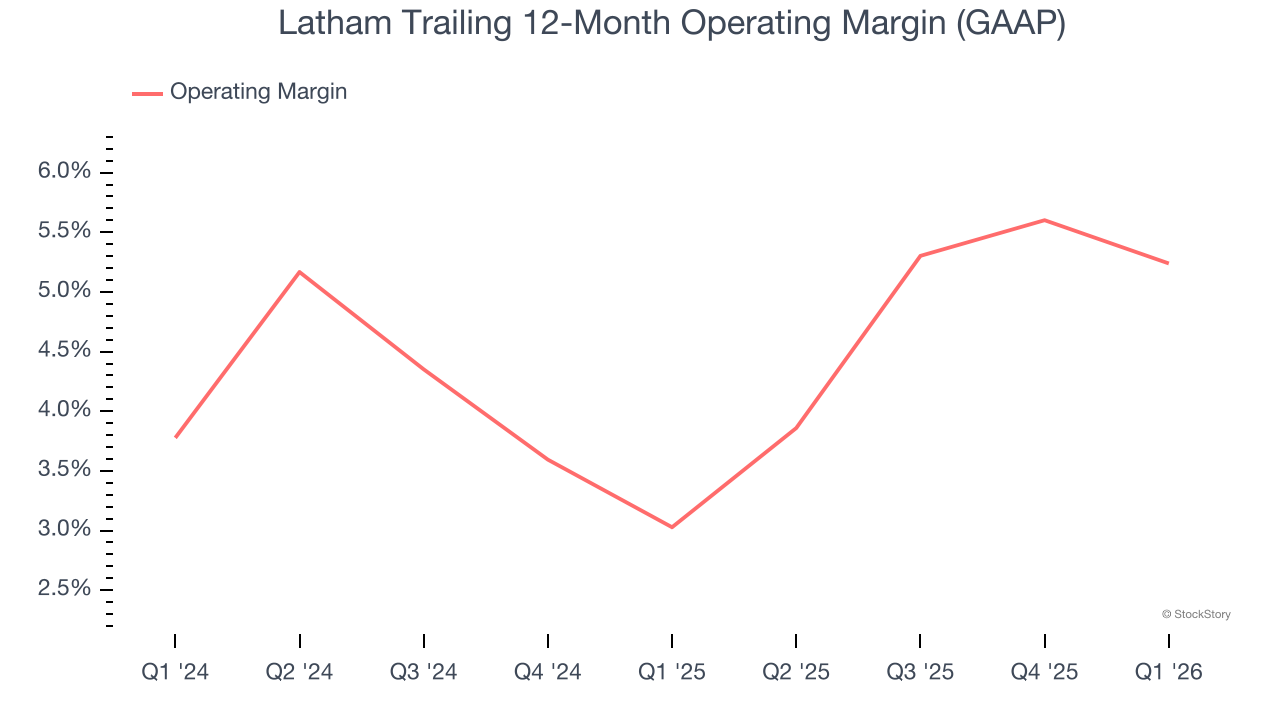

Operating Margin

Latham’s working margin has been trending up over the past 12 months and averaged 4.2% over the past two years. The firm’s greater effectivity is a breath of recent air, however its suboptimal price construction means it nonetheless sports activities insufficient profitability for a client discretionary enterprise.

In Q1, Latham generated an working margin revenue margin of detrimental 5.6%, down 1.2 share factors 12 months on 12 months. This discount is kind of minuscule and signifies the corporate’s total price construction has been comparatively steady.

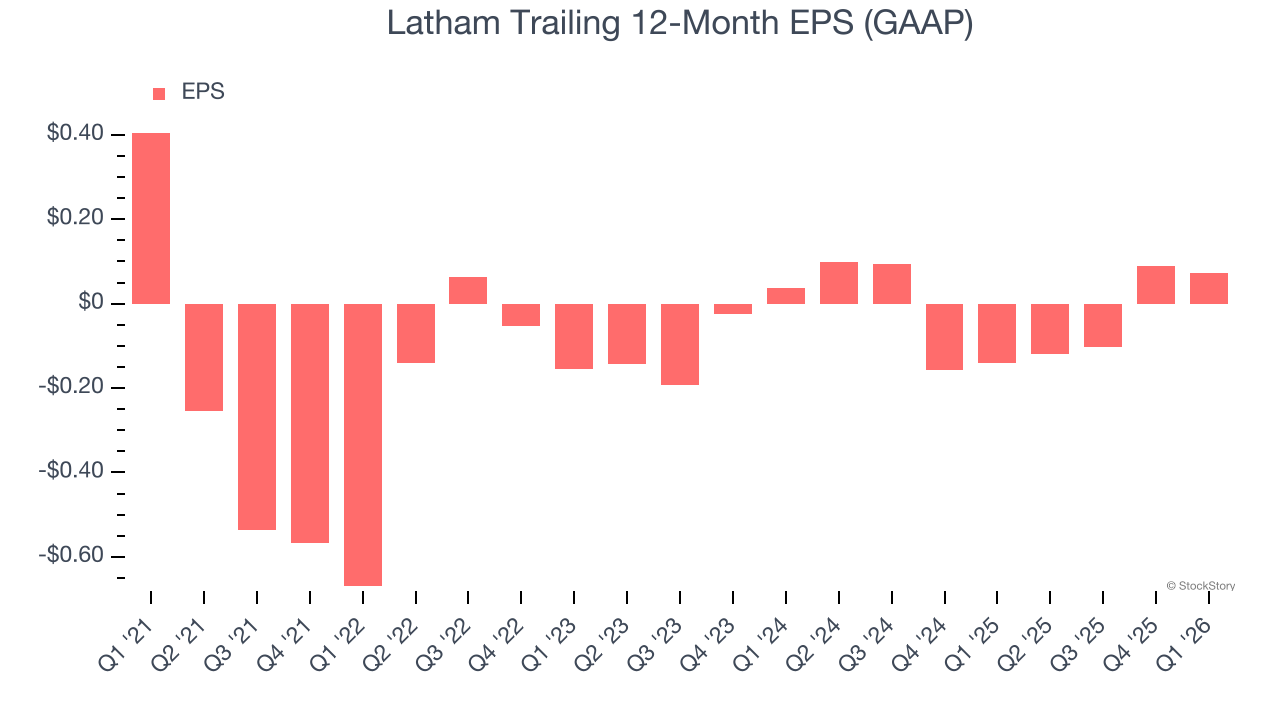

Earnings Per Share

Revenue developments clarify an organization’s historic progress, however the long-term change in earnings per share (EPS) factors to the profitability of that progress – for instance, an organization might inflate its gross sales by extreme spending on promoting and promotions.

Sadly for Latham, its EPS declined by 29.3% yearly over the past 5 years whereas its income grew by 2%. This tells us the corporate turned much less worthwhile on a per-share foundation because it expanded on account of non-fundamental elements equivalent to curiosity bills and taxes.

In Q1, Latham reported EPS of detrimental $0.07, down from detrimental $0.05 in the identical quarter final 12 months. Despite falling 12 months on 12 months, this print beat analysts’ estimates by 2.9%. Over the subsequent 12 months, Wall Street expects Latham’s full-year EPS of $0.07 to develop 116%.

Key Takeaways from Latham’s Q1 Results

It was encouraging to see Latham’s full-year EBITDA steering beat analysts’ expectations. We had been additionally glad its full-year income steering was according to Wall Street’s estimates. On the opposite hand, its adjusted working earnings missed and its income fell in need of Wall Street’s estimates. Overall, this was a weaker quarter. The inventory remained flat at $5.86 instantly following the outcomes.

Is Latham a horny funding alternative on the present value? When making that call, it’s essential to contemplate its valuation, enterprise qualities, in addition to what has occurred within the newest quarter. We cowl that in our actionable full analysis report which you’ll be able to learn right here (it’s free).

This web page was created programmatically, to learn the article in its authentic location you possibly can go to the hyperlink bellow:

https://stockstory.org/us/stocks/nasdaq/swim/news/earnings/latham-nasdaqswim-reports-sales-below-analyst-estimates-in-q1-cy2026-earnings

and if you wish to take away this text from our website please contact us